Insurance Claim Recovery Support

Licensed Public Adjusters

What Is A Public Adjuster?

Trusted By Property Owners Nationwide

Homeowners | Apartment Owners | HOA Boards | Commercial Property Owners | Churches | Nonprofits

Learn how public adjusters help homeowners, commercial property owners, HOAs, apartment operators, religious organizations, and nonprofits recover the full amount owed under their insurance policies.

A Complete Guide for Homeowners & Business Property Owners Facing Property Damage Insurance Claims.

90-Second Video Highlights

What Is A Public Adjuster?

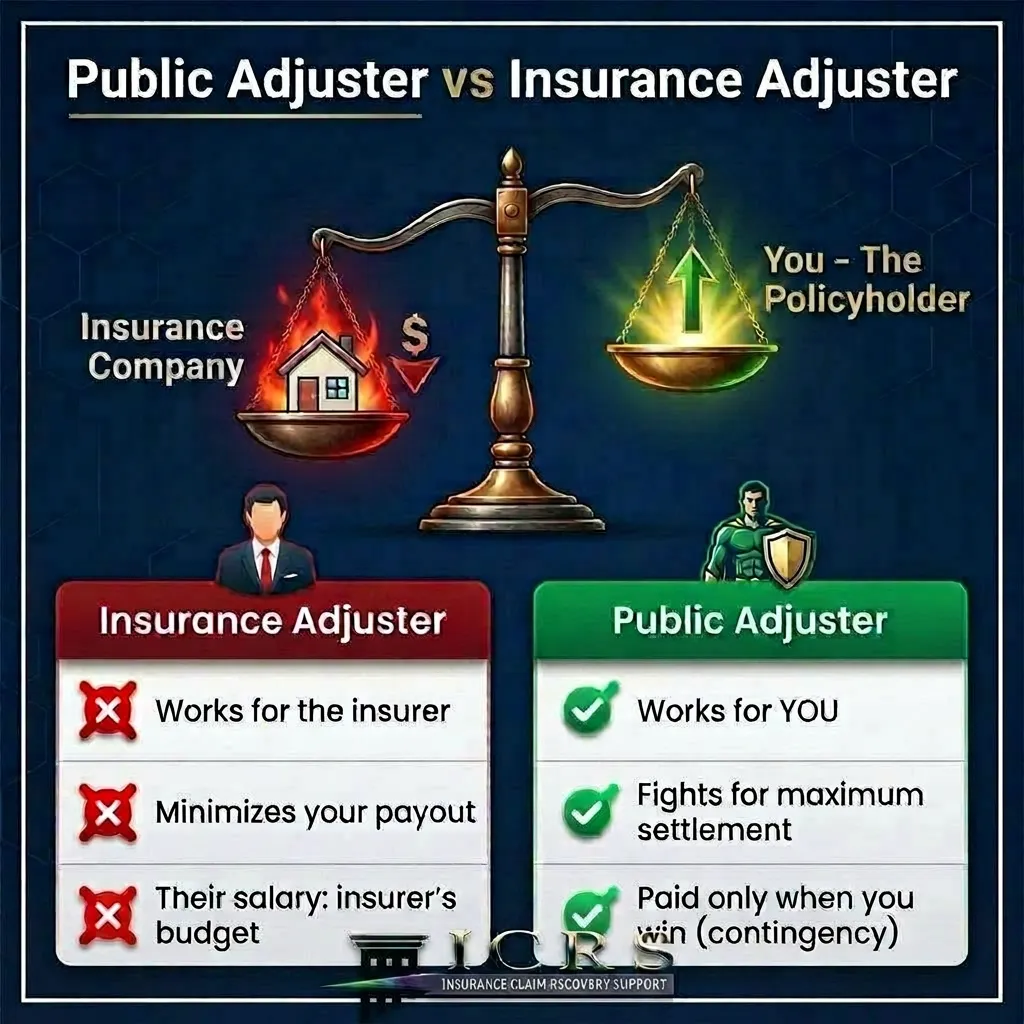

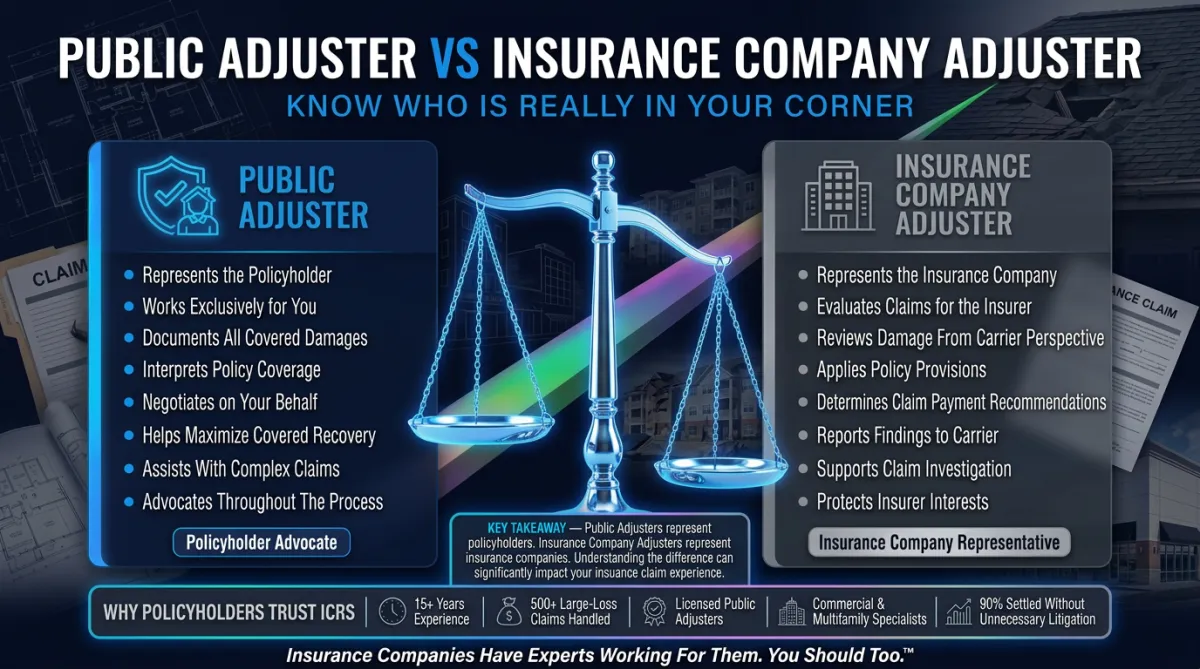

A public adjuster is a licensed insurance professional who represents policyholders—not insurance companies. They help document property damage, interpret insurance policies, prepare claims, and negotiate settlements. Public adjusters work to ensure homeowners, business owners, HOAs, apartment owners, and other policyholders receive the full benefits available under their insurance policies.

Who Hires Public Adjusters?

Public adjusters are hired by homeowners, condominium associations, apartment owners, commercial property owners, property managers, nonprofits, and religious organizations. They are often brought in after fire, storm, hail, hurricane, water damage, or business interruption losses when policyholders need experienced representation during the claims process.

What Claims Do Public Adjusters Handle?

Public adjusters handle property damage claims involving fire, smoke, hail, wind, hurricanes, tornadoes, water damage, roof damage, vandalism, and business interruption losses. They also assist with disputes involving claim underpayments, coverage interpretations, repair costs, code upgrades, and loss of income related to insured property damage.

How Do Public Adjusters Get Paid?

Most public adjusters work on a contingency-fee basis, meaning they are paid only if they recover money for the policyholder. Their fee is typically a percentage of the insurance settlement, allowing property owners to obtain professional representation without large upfront costs during the claims process.

Trusted by 1,000+ clients worldwide

Key Takeaways

Public adjusters represent policyholders, not insurance companies.

Insurance company adjusters represent the insurer.

Policyholders generally bear the burden of proving their claim.

Insurance companies must investigate and evaluate claims in good faith.

Public adjusters help document damages and negotiate settlements.

Property owners have a duty to mitigate further damage after a loss.

Why Property Owners Trust ICRS

🏆 15+ Years Experience

🏢 500+ Large-Loss Claims Handled

⚖️ 90% Settled Without Unnecessary Litigation

🛡️ Licensed Public Adjusters

🏘️ Commercial & Multifamily Specialists

💰 Millions Recovered For Policyholders

What Is A Public Adjuster?

🛡️ Quick Answer

A public adjuster is a licensed insurance professional who represents policyholders—not insurance companies—during the insurance claim process.

Public adjusters help document damages, interpret insurance policies, prepare claims, and negotiate settlements to help policyholders pursue the full benefits available under their coverage.

Key Takeaways

✓ Works for the policyholder

✓ Not employed by the insurance company

✓ Helps document and value damages

✓ Negotiates claim settlements

✓ Advocates for property owners

Understanding The Different Types Of Adjusters

⚖️ Quick Answer

Not all adjusters work for the policyholder.

There are three primary types of adjusters involved in property insurance claims.

1. Insurance Company Adjuster

Represents the insurance company.

Their job is to investigate claims and evaluate what the insurer believes may be owed.

2. Independent Adjuster

Hired by the insurance company.

Works on behalf of the insurer but is not a direct employee.

3. Public Adjuster

Represents the policyholder.

Advocates exclusively for the insured throughout the claim process.

Key Takeaway

The public adjuster is the only adjuster specifically hired to represent the policyholder's interests.

Why Do People Hire Public Adjusters?

📋 Quick Answer

Most policyholders have never handled a large insurance claim.

Public adjusters help navigate the process and advocate for the property owner.

Common Reasons People Hire Public Adjusters

🔥 Fire Damage

🌪️ Tornado Damage

🧊 Hail Damage

💨 Wind Damage

🌊 Water Damage

🏠 Roof Damage

🚰 Burst Pipe Losses

🏢 Commercial Property Damage

💼 Business Interruption Losses

Key Takeaway

Many policyholders seek help after a claim has been delayed, underpaid, partially denied, or becomes too complex to manage alone.

The Policyholder Bears The Burden Of Proof

📑 What You Need To Know

In most property insurance claims, the policyholder has the responsibility to prove their loss.

Policyholders Must Demonstrate

✓ A covered loss occurred

✓ The extent of the damage

✓ The cost to repair or replace damaged property

✓ Additional covered losses

✓ Compliance with policy requirements

Key Takeaway

The quality of your documentation often influences the outcome of your claim.

The Duty To Mitigate Damages

🏠 What You Need To Know

Insurance policies generally require property owners to take reasonable steps to prevent additional damage after a loss.

Examples

✓ Roof tarping

✓ Board-up services

✓ Water extraction

✓ Structural stabilization

✓ Temporary repairs

Key Takeaway

Failure to mitigate damages can create additional claim disputes.

Understanding Indemnity

⚖️ What Is Indemnity?

Insurance is designed to restore policyholders to their pre-loss condition.

The goal is to make the insured whole again—not better and not worse.

Common Indemnity Issues

✓ Partial roof replacements

✓ Matching concerns

✓ Code upgrades

✓ Depreciation disputes

✓ Lost rental income

✓ Business interruption losses

Key Takeaway

Proper claim documentation helps support a policyholder's pursuit of full indemnification.

The Insurance Company's Duty Of Good Faith

🛡️ What You Need To Know

Insurance companies are generally required to investigate and evaluate claims fairly.

Good Faith Responsibilities

✓ Conduct reasonable investigations

✓ Consider all available evidence

✓ Communicate honestly

✓ Process claims promptly

✓ Make fair coverage decisions

Key Takeaway

Insurance companies should evaluate evidence that supports coverage as fairly as evidence that may limit it.

What Does A Public Adjuster Actually Do?

🔍 Core Services

Policy Review

Analyze policy language and available coverages.

Damage Assessment

Inspect and document damages.

Claim Preparation

Prepare estimates, inventories, and supporting documentation.

Claim Management

Coordinate inspections and communications.

Negotiation

Negotiate claim values and settlements.

Settlement Review

Help evaluate settlement offers.

Key Takeaway

The objective is to ensure no covered damage is overlooked or undervalued.

Who Can Benefit From Hiring A Public Adjuster?

🏢 Who We Help

🏠 Homeowners

🏘️ Condominium Associations

🏡 HOA Boards

🏢 Apartment Building Owners

📋 Property Management Companies

🏬 Commercial Property Owners

⛪ Religious Organizations

❤️ Nonprofit Organizations

Key Takeaway

Public adjusters assist a wide variety of policyholders facing property damage and business interruption losses.

Is Hiring A Public Adjuster Worth It?

💡 Quick Answer

Every claim is different.

Many policyholders choose professional representation because insurance claims can involve significant financial stakes and complex policy issues.

Public Adjusters Provide Expertise In

✓ Policy interpretation

✓ Construction estimating

✓ Damage documentation

✓ Claim preparation

✓ Settlement negotiations

Key Takeaway

For many property owners, professional representation provides confidence, expertise, and advocacy during a stressful claim process.

The Bottom Line

🎯 What You Should Remember

A public adjuster is a licensed insurance professional who works exclusively for policyholders.

Whether the loss involves a home, apartment complex, condominium association, commercial building, church, nonprofit facility, or business, public adjusters help property owners document damages, prepare claims, and negotiate settlements.

Final Takeaway

Before accepting an insurance settlement, make sure you fully understand your policy, your damages, and your options.

Hear What Our Clients Are Saying

Thank you Scott!

Scott responded to my inquiry and took the time to listen and understand our unpleasant experience dealing with our insurance claim. Although I did not utilized his service, he gave me a sound, professional advice and offered to help when he referred me to his engineer. They replied promptly and I was able to have better understanding of the situation. Thank you Scott! - Haidee J.

I would highly reccomend!

Words can’t describe how grateful we are for the consultation and claim evaluation we had with Scott. Full disclosure we were unable to work with him due to limitations of our scope. We wanted to properly recognize Scott for the honest and genuine passion he put in to not only our claim, but the way he runs his business in general. We hadn’t had such clarity of next steps since this began in 2020. I would highly recommend this business to everyone spinning their wheels in this process!

- James M.

I came across this company and had none of those bad feelings!

This was not the first public adjuster I called. I called a different company first but they gave me a bad feeling on the phone. Too aggressive. Didn't feel trustworthy to me. So, I kept looking. I came across this company and I had none of those bad feelings. Scott, the guy who took my call, seemed very knowledgeable and I felt I could fully trust him. As it turned out, he told me that my claim was fairly simple and I didn't need the full scope of his service and fees. - Katie H.

What Is A Public Adjuster?

"The Complete Policyholder's Guide to Navigating Property Insurance Claims"

Get the Insider’s Guide the Insurance Companies Hope You Never Read

Discover How to Protect Your Claim, Maximize Your Settlement & Avoid Being Underpaid

What You’ll Discover Inside

How the insurance claim process really works

Step-by-step breakdowns for both residential and commercial claims.

Why insurers deny, delay, or underpay claims

And how to protect yourself from common tactics.

How public adjusters help increase settlement amounts

Including real examples of claims that went from tens of thousands to hundreds of thousands.

Claim documentation tips

Photos, logs, reports, and evidence insurance companies can’t ignore.

Business & commercial claim strategies

Business Interruption (BI), Extra Expense (EE), equipment, inventory loss, and tenant issues.

How to overcome disputes and denials

Appraisal, mediation, ROR responses, and bad faith indicators.

Checklists, templates & tools

Claim diary, ALE log, BI worksheet, inventory lists, communication templates, and more.

Why You Need This Guide — Now More Than Ever

Public adjusters work for policyholders, not insurers. Their loyalty and compensation are aligned with your best outcome.

Insurers are paying out less, scrutinizing more, and relying on overwhelmed or inexperienced adjusters — especially after big storms, fires, or catastrophic events. The result...

Claims take longer

Settlements are smaller

Denials are more common

Policyholders are left confused and frustrated

Get knowledge and strategies to take back control. Policyholders with professional representation recover significantly more.

About the Author

This guide is based on the experience of Scott Friedson, a licensed public adjuster and founder of Insurance Claim Recovery Support, specializing in commercial and large-loss insurance claims.

Over the past 15+ years, Scott has helped property owners navigate complex claims involving commercial buildings, multifamily properties, and high-value assets—often resolving claims without unnecessary litigation.

Table of Contents

What Is A Public Adjuster?

Understanding The Different Types Of Adjusters

Why Policyholders Hire Public Adjusters

The Policyholder's Burden Of Proof

The Duty To Mitigate Damages

Understanding Indemnity

The Insurance Company's Duty Of Good Faith

What Public Adjusters Actually Do

Common Insurance Claim Disputes

Fire Damage Claims

Storm Damage Claims

Business Interruption Claims

Commercial Property Claims

Multifamily Property Claims

Frequently Asked Questions

When To Hire A Public Adjuster

Next Steps After A Loss

BONUS GUIDE

The Iron Gut of a Public Adjuster

"Inside the Relentless Mindset Behind Successful Insurance Claim Recovery"

What You’ll Discover Inside

Table of Contents

Introduction: Why Public Adjusters Need An Iron Gut

From Ground Zero To Boardroom Battles

Into The Aftermath: Assessing Damage In Disaster Zones

The Psychological Gauntlet

Negotiating With Billion-Dollar Insurance Companies

Mastering The Maze Of Policy Language

Persistence Through Delays And Denials

Delivering Justice And Financial Recovery

The Quiet Hero In A Complex System

How ICRS Helps Policyholders

You Need This Guide — Now More Than Ever

Public adjusters work for policyholders, not insurers. Their loyalty and compensation are aligned with your best outcome.

About the Author

This guide is based on the experience of Scott Friedson, a licensed public adjuster and founder of Insurance Claim Recovery Support, specializing in commercial and large-loss insurance claims.

Over the past 15+ years, Scott has helped property owners navigate complex claims involving commercial buildings, multifamily properties, and high-value assets—often resolving claims without unnecessary litigation.

Bonus Included: The Iron Gut Of A Public Adjuster

Guide #1: Teaches you what a public adjuster does.

Guide #2: Shows you what it takes to stand up to billion-dollar insurance companies.

TYPE OF ADJUSTER

Public Adjuster

Company Adjuster

Independent Adjuster

General Adjuster

WHO THEY WORK FOr

Policyholder

Insurance Company

Insurance Company

Insurance Company

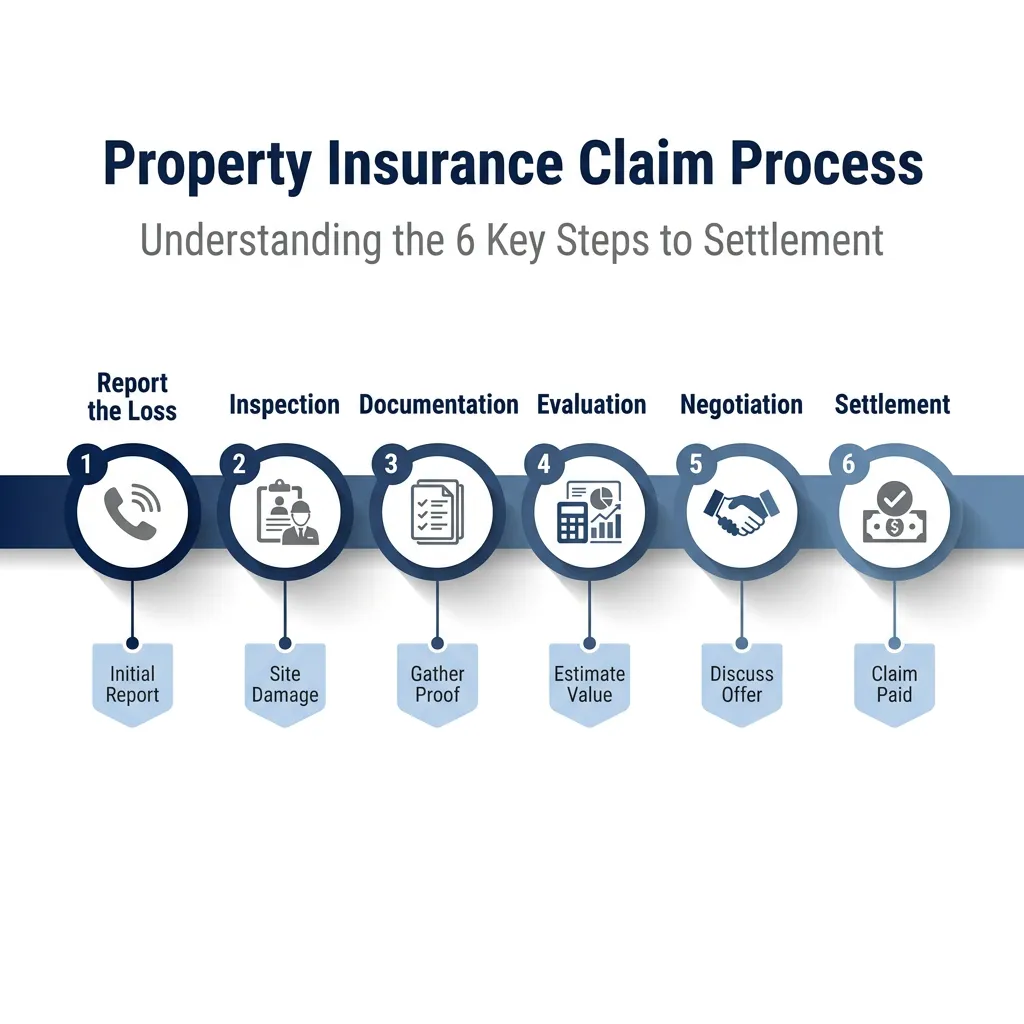

The Insurance Claim Recovery Process:

What You Need to Know

Burden of Proof

As the policyholder, you bear the burden of proof, you must clearly demonstrate the loss is covered under your policy. However, if your insurer cites exclusions to deny coverage, they must prove those exclusions apply.

Duty to Mitigate

You’re legally required to mitigate further damage. This means taking reasonable steps (e.g., temporary repairs or boarding up) to prevent worsening of loss.

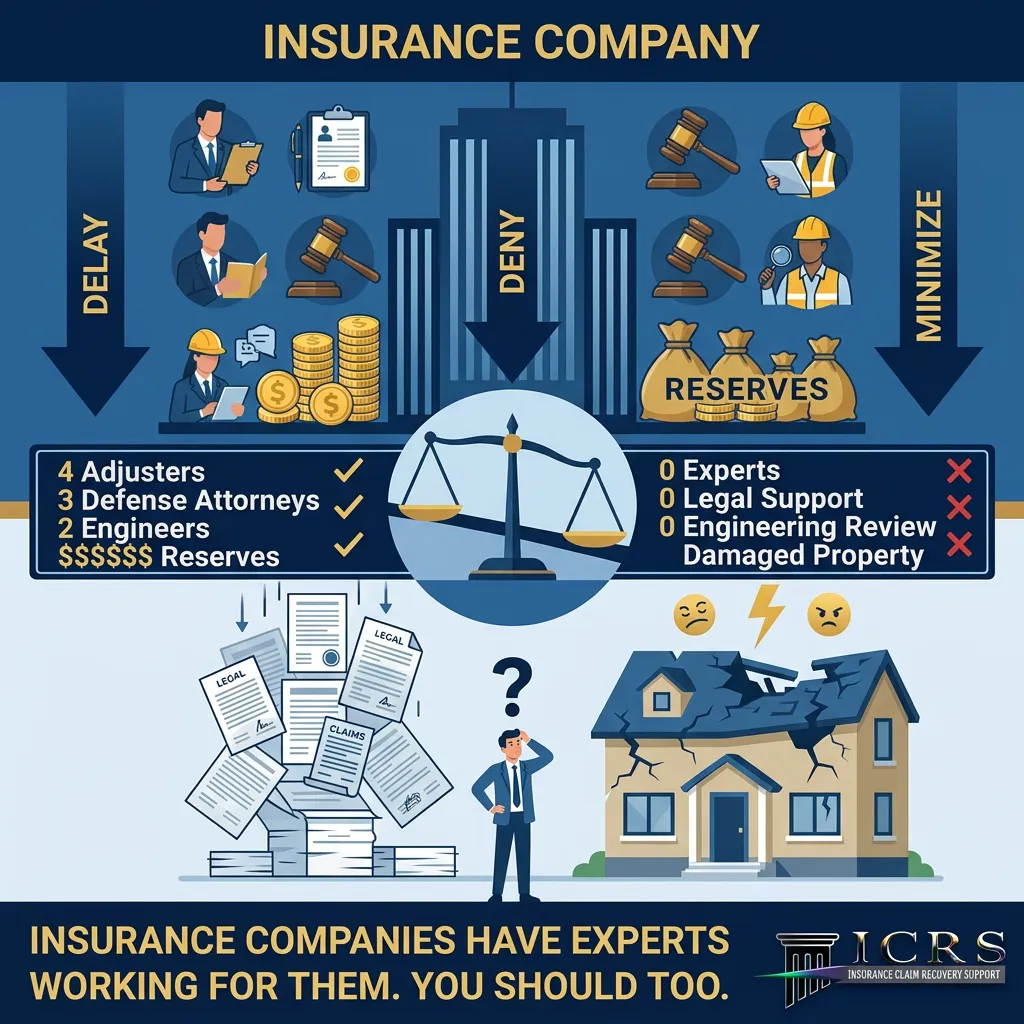

Insurers Have the Advantage.

They wrote the policy, have your money, deploy adjusters, engineers, and lawyers to represent their interests, not yours; public adjusters help level the field for policyholders.

10%–747%+ Increase

Studies show, settlements are significantly higher with public adjusters.

Early Involvement Matters.

Bringing in a public adjuster at the start prevents documentation gaps and denial risks.

Documentation is Power.

Photos, receipts, logs, and written communication strengthen any claim.

Patience Pays

Bringing in a public adjuster at the start prevents documentation gaps and denial risks.

Fairness and Peace of Mind.

You don’t have to fight alone. Having a knowledgeable advocate ensures you get the settlement you deserve.

Good Faith and Indemnity

Insurance is built on the doctrine of indemnity, meaning you should be restored to your pre-loss condition, not profit. Companies owe you a duty of utmost good faith, treating evidence in your favor with the same consideration as theirs.

Bad Faith by Insurers

If your insurer unreasonably delays, denies, or devalues your claim, you may have a bad faith claim. You must prove their misconduct, like ignoring evidence or dragging out the process, often with documentation, correspondence, or expert reports . Remedies can include the policy amount, additional compensatory damages, attorney’s fees, and even punitive damages.

Frequently Asked Questions

What is a public adjuster?

A public adjuster is a licensed insurance professional hired by a property owner to represent their interests in appraising and negotiating an insurance claim. Unlike a company or independent adjuster, who works for the insurance company, a public adjuster works solely for the policyholder to help them receive a fair settlement.

What does a public adjuster do?

A public adjuster evaluates damage, prepares detailed claim documentation, communicates with the insurance company, and negotiates the settlement on behalf of the policyholder.

How is a public adjuster different from an insurance company adjuster?

A public adjuster works exclusively for the policyholder, while insurance company adjusters represent the insurer’s interests. Public adjusters focus on maximizing your claim; company adjusters focus on minimizing payout.

When should you hire a public adjuster?

Hire a public adjuster when the damage is significant, the claim is complicated, the insurance company is delaying or underpaying, or when you want expert representation from the start.

How do public adjusters get paid?

Most public adjusters work on a contingency fee—typically a percentage of the settlement—so they only get paid if you get paid.

Do public adjusters get higher settlements?

Yes. Studies and industry data show policyholders often receive larger settlements when represented by a public adjuster due to better documentation, valuation, and negotiation.

What types of claims do public adjusters handle?

They handle property damage claims from fire, hail, wind, tornado, hurricane, water, vandalism, business interruption, and large-loss commercial claims.

Can a public adjuster help if my claim is denied or underpaid?

Yes. Public adjusters can reopen, supplement, and negotiate denied or underpaid claims to pursue the amount you’re owed.

Are public adjusters licensed?

Yes. Public adjusters must hold a state license, follow strict regulations, and meet ongoing education and ethical requirements.

How do I find a reputable public adjuster?

Look for a licensed, experienced public adjuster with strong reviews, industry credentials, and a proven track record handling claims similar to yours.

Who is this guide for?

Homeowners

Facing fire, water, hurricane, hail, or storm damage.

Business Owners

Struggling with BI, EE, equipment damage, or forced closures.

HOAs, Religious Organizations, Commercial & Multifamily Property Managers

Managing complex losses, roof systems, water intrusion, and building envelope claims.

Contractors & Restoration Pros

Looking to help clients navigate insurance claims more effectively.

Any Policyholder Who Wants to Avoid Being Underpaid by Their Insurance Company

Condo associations

Commercial building owners

Churches, schools, and religious groups

Apartment complex owners

Syndicators

Property management companies

Nonprofits with insured property

Real Estate Investors

Insurance Brokers

Contractors

Roofers

Restoration Contractors

Why can’t I just trust the insurance company adjuster?

Because they work for the insurer — not you. Their job is to minimize what’s paid. You need your own advocate.

What’s the biggest mistake policyholders make?

Accepting the first settlement or waiting too long. Delays can ruin your ability to get paid fairly.

When should a policyholders hire a Public Adjuster?

Engaging a public adjuster early in the process for Large-Loss claims offers critical advantages.

Should I hire a public adjuster or handle the claim myself?

You can handle it yourself, but public adjusters typically achieve better outcomes and reduce the stress, time, and risk of mistakes that can cost you money.

What is a "Good" public adjuster?

As soon as you download our free guide, you will be shown a brief video that answers that question.

What does a public adjuster do?

A public adjuster is a licensed insurance professional who represents policyholders—not insurance companies—during the insurance claim process. Public adjusters help document damages, review insurance policies, prepare detailed claim estimates, gather supporting evidence, and negotiate settlements with the insurance company on behalf of the insured.

Unlike insurance company adjusters, who work for the insurer, public adjusters work exclusively for homeowners, apartment owners, condominium associations, HOA boards, commercial property owners, churches, nonprofits, and property management companies.

Public adjusters commonly assist with fire damage, storm damage, hail claims, hurricane losses, water damage, business interruption losses, and large commercial property claims. Their goal is to help ensure all covered damages are identified, documented, and properly presented so policyholders can pursue the full benefits available under their insurance policy.

Are Public Adjusters Worth It?

For many policyholders, hiring a public adjuster can be one of the most important decisions made during a property insurance claim. Insurance claims often involve complex policy language, hidden damages, construction estimating, code requirements, depreciation issues, and extensive documentation requirements.

Many property owners only experience a major insurance claim once or twice in their lifetime, while insurance companies handle claims every day. A public adjuster brings experience, expertise, and advocacy to help level the playing field.

Whether a public adjuster is worth hiring depends on the size and complexity of the claim. For large losses, disputed claims, underpaid claims, business interruption losses, or situations involving extensive property damage, professional representation can help policyholders better understand their rights, responsibilities, and available coverages.

How Much Does a Public Adjuster Cost?

Most public adjusters are compensated through a contingency fee, meaning they are paid a percentage of the insurance settlement they help recover for the policyholder. If there is no recovery, there is generally no fee.

Fee structures vary by state and may be regulated by state law. The percentage can depend on factors such as claim size, claim complexity, timing of engagement, and applicable state regulations.

At Insurance Claim Recovery Support (ICRS), claims involving more than $250,000 in damages after deductible are typically handled on a contingency basis. For smaller claims, policyholders may benefit from ClaimNavigator, which provides professional claim guidance and support for a nominal flat fee with a 100% satisfaction guarantee.

Before hiring any public adjuster, policyholders should understand the fee agreement, services provided, and applicable state regulations.

Should I Hire a Public Adjuster After a Fire?

Fire claims are among the most complex property insurance claims. In addition to structural damage, fire losses often involve smoke damage, soot contamination, water damage from firefighting efforts, code upgrade requirements, personal property inventories, business interruption losses, and additional living expenses.

A public adjuster can help document all areas of damage, prepare detailed estimates, review policy provisions, and negotiate with the insurance company regarding scope, pricing, and coverage issues.

Because fire losses frequently involve substantial financial exposure and multiple categories of coverage, many homeowners, apartment owners, commercial property owners, churches, and nonprofit organizations choose to seek professional representation to help manage the claim process and protect their interests.

Should I Hire a Public Adjuster After Hail Damage?

Hail claims often appear straightforward but can involve significant disputes regarding roof damage, siding damage, HVAC systems, gutters, windows, building components, and code compliance requirements.

Insurance companies and policyholders may disagree regarding:

- Whether hail damage exists

- The extent of damage

- Repair versus replacement

- Matching requirements

- Building code upgrades

- Scope of repairs

A public adjuster can assist by documenting damage, reviewing engineering reports, obtaining expert inspections, preparing estimates, and negotiating with the insurance company.

This is especially important for apartment complexes, condominium associations, commercial buildings, churches, and multifamily properties where damages can be extensive and repair costs substantial.

Can a Public Adjuster Reopen a Claim?

In some situations, yes.

Many insurance claims can be reopened when additional damages are discovered, supplemental repairs become necessary, hidden damages are uncovered, or previously unknown costs arise during reconstruction.

The ability to reopen a claim depends on:

- Policy language

- State law

- Claim status

- Applicable deadlines

- Newly discovered damages

A public adjuster can review the claim file, evaluate the circumstances, and determine whether additional benefits may still be available.

If you believe your claim was underpaid or important damages were overlooked, it may be worthwhile to have the claim reviewed before assuming the claim is permanently closed.

Can a Public Adjuster Help With Business Interruption?

Yes.

Business interruption claims are often among the most complex aspects of a commercial property insurance claim.

These claims may involve:

- Lost income

- Lost rents

- Continuing operating expenses

- Extra expenses

- Tenant disruptions

- Reduced occupancy

- Delayed reopening costs

Calculating business interruption losses frequently requires detailed financial analysis, documentation, accounting records, and policy interpretation.

Public adjusters often work alongside accountants, consultants, property owners, and business operators to help quantify losses and present them to the insurance company.

For apartment owners, commercial property owners, churches, nonprofits, and businesses, business interruption coverage can represent a substantial portion of the overall claim value.

What Happens If My Claim Is Underpaid?

If you believe your insurance claim has been underpaid, you may have several options depending on your policy, state law, and claim circumstances.

Common signs of an underpaid claim include:

- Missing damage items

- Incomplete repair estimates

- Excessive depreciation

- Disputed scope of repairs

- Denied building code upgrades

- Insufficient business interruption calculations

- Settlement amounts that do not restore the property to its pre-loss condition

Policyholders are not always required to accept the insurance company's initial offer.

A public adjuster can review the policy, estimate, claim documentation, and settlement offer to identify potential gaps or overlooked damages. In many cases, supplemental documentation, expert reports, additional inspections, or negotiations may help resolve disputes and pursue additional recovery.

Before accepting any settlement, it is important to understand what your policy covers, whether all damages have been documented, and whether the proposed payment accurately reflects the true cost of recovery.

What Is a Public Adjuster? How Public Adjusters Help Insurance Claims

Learn what a public adjuster does, how public adjusters help policyholders navigate property damage insurance claims, and why commercial property owners, multifamily operators, and businesses seek exp... ...more

Public Adjusters

May 18, 2026•18 min read

Insurance Claim Recovery Support

Licensed Public Insurance Adjusters

Start Claim Review | Claim Results | What Is a Public Adjuster | Insurance Claim Bible

Fire Claim Guide | Hail & Wind Claim Guide | Roof Claim Guide | Hurricane Claim Guide | Hail Insurance Claims | Stop Crooked Contractors

NAIC | Insurance Information Institute

© Insurance Claim Recovery Support. All rights reserved.